30 Jul , 2025 By : Debdeep Gupta

Sun Pharmaceutical Industries is set to announce its Q1FY26 results on August 1, with analysts expecting a steady topline and bottom-line performance supported by strong India growth and sequential improvement in the US specialty business. However, higher investments towards product launches and R&D are likely to exert some pressure on margins.

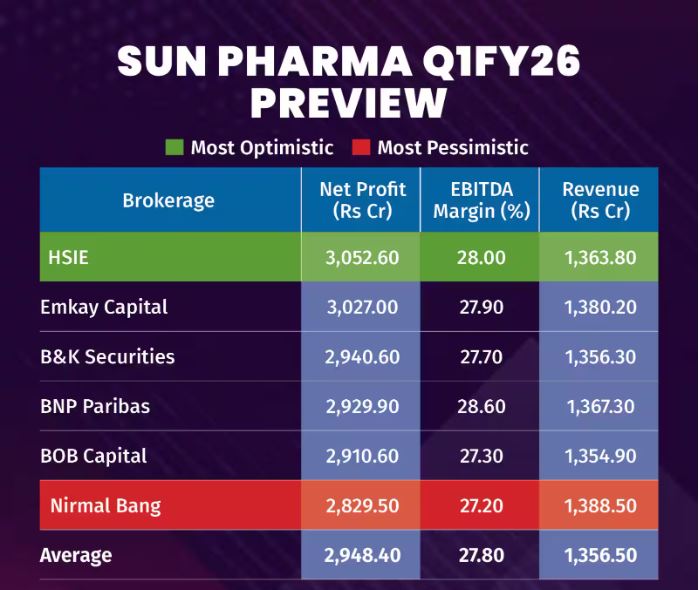

According to a Moneycontrol poll, Sun Pharma’s consolidated revenue is estimated to grow 8 to 9 percent year-on-year (YoY) to around Rs 13,500 to 13,800 crore, while net profit is seen rising 2 to 7 percent YoY to about Rs 2,900 to 3,050 crore. EBITDA is expected to come in the range of Rs 3,700 to 3,910 crore, with margin likely to decline slightly by 10 to 90 basis points YoY.

BNP Paribas' revenue estimates, as mentioned in its note, are in line with consensus, while EBITDA is marginally higher, considering launch-related costs will ramp up from Q2 onwards. It went on to add that the full impact of two specialty product launches — Leqselvi and Unloxcyt — is likely to be felt in subsequent quarters.

There is a narrow divergence in earnings estimates across brokerages, so any deviation from consensus could trigger sharp stock movement.

What factors are likely to drive its earnings?

Sun Pharma’s growth in Q1 is seen as broad-based but measured, with domestic formulations, US specialty sales, and some support from gRevlimid driving topline expansion. However, these gains could be partly offset by foreign exchange losses and higher launch-related costs.

Sun Pharma is expected to deliver healthy double-digit domestic growth for an eighth consecutive quarter, according to Emkay Global's latest note. Thus, projecting a 10.5 percent YoY rise in India revenue, aided by strong performance in chronic and specialty segments.

HSIE concurs, highlighting traction in chronic, CNS and specialty products, and adds that Sun is likely to outperform IPM’s \~7.2 percent growth, partly due to its branded chronic exposure.

India business: Expected to grow 10 to 12 percent YoY, driven by volume gains, in-licensing deals, and new launches. Price hikes and medical rep expansion have also aided productivity, noted B\&K Securities.

US business: Sales may rise 5 to 6 percent QoQ to about USD 460 to 488 million, supported by stable gRevlimid contribution and higher specialty sales, including Ilumya and Winlevi. Emkay estimates specialty revenue at USD 310 million, up from USD 295 million last quarter. However, the overall US market remains volatile amid channel stocking and pricing pressure.

While Sun Pharma guided for USD 100 million of launch costs for new specialty products, we believe Q1 margins will remain stable with pressure emerging in later quarters, BNP Paribas noted.

gRevlimid: Contribution expected to improve QoQ but remain lower YoY due to intensified competition. According to BOB Capital, Revlimid-linked growth is tapering, and gRevlimid sales are unlikely to be offset by new approvals in the near term.

Margins: EBITDA margin may see a 10 to 90 bps YoY contraction, largely due to elevated R&D and forex losses. Sun incurred an estimated Rs 505 crore forex loss during the quarter, as per B&K Securities.

What to watch out for in the quarterly show?

Analysts will be keenly watching Sun’s commentary on its specialty portfolio, the ramp-up of newly launched drugs, and any guidance on margin trajectory, especially with USD 100 million in launch costs expected to reflect more meaningfully in Q2 onwards.

Further, updates on US pricing dynamics, progress in pipeline drugs, and commentary around the tariff environment for pharma exports will be closely tracked.

Sun Pharma remains one of our top picks in the sector, driven by its robust India franchise and differentiated US portfolio, mentions Nirmal Bang's latest note. It also cautioned that cost normalisation and price erosion in generics could act as a headwind.

0 Comment