28 Apr , 2025 By : Debdeep Gupta

Reliance Industries Ltd’s (RIL’s) shares jumped 3 percent in early trading on April 28 to emerge as the top gainer on the Nifty 50 index, after the Mukesh Ambani-led company beat earnings estimates for the fiscal quarter ended March.

The company's net profit attributable to shareholders grew 2.4 percent to Rs 19,407 crore for Q4 FY25, beating Street expectations, as a result of lower depreciation, interest and tax rate. Revenue for the three months ended March 31 climbed 8.8 percent from a year ago to Rs 2.88 lakh crore, driven by company’s digital services, retail and oil-to-chemicals business.

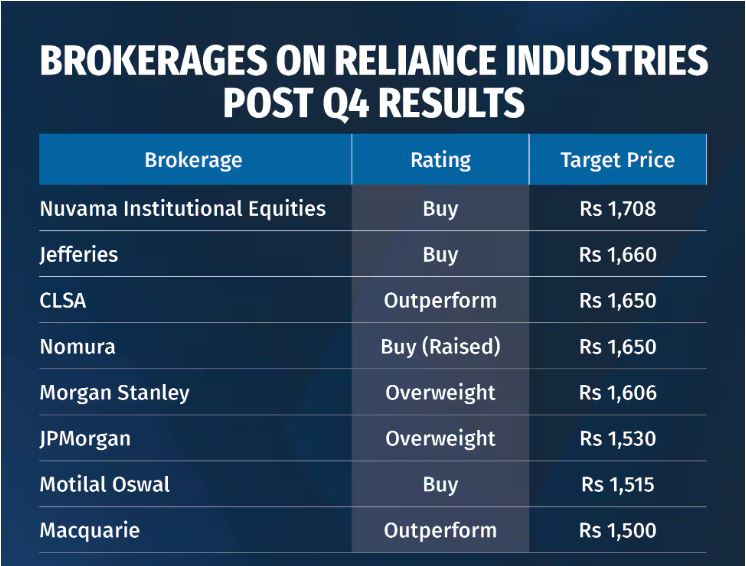

Brokerages hiked their target prices on the Nifty 50 heavyweight following its March quarter earnings report, as a result of its robust performance across segments and higher-than-anticipated results for the O2C segment.

At 9.40 am, shares of Reliance Industries surged 3 percent to quote Rs 1,339.60 apiece on the NSE.

The bullishness on RIL shares was largely driven by the telecommunication arm Reliance Jio. Domestic brokerage Motilal Oswal said, segment-wise, it expects Jio to be the biggest growth driver with 21 percent annual EBITDA growth over FY25-27, driven by one more tariff hike, market share gains in wireless, and ramp-up of the homes and enterprise business.

Japan’s Nomura Holdings noted a few key triggers which will drive growth for Reliance Industries in the near term: scale-up of the new energy business, upcoming tariff hikes for Jio, and potential IPO/listing for Jio, which will drive value-unlocking for RIL.

“Additionally, with the completion of streamlining of operations at Reliance Retail, the retail business will sustain a healthy growth trajectory,” Nomura said.

JPMorgan also noted the sharp acceleration of Reliance Retail’s growth in Q4, jumping 16 percent year-on-year. The brokerage noted, with favourable valuations, that this could contribute to the share price in the near term.

On the new energy front, Nuvama Institutional Equities estimates that the PAT share could jump to 12 percent by FY2030, especially given the management’s expectations of the new energy segment equaling the O2C segment’s profit by FY2031. Further, the brokerage said that new energy should add over 50 per cent of current additions to the consolidated net profit amid the higher value afforded to ‘clean’ technology.

“Overall, we build in a CAGR of ~13-14 percent in consolidated EBITDA and PAT over FY25-27, driven by a double-digit EBITDA CAGR in RJio and Retail. After a subdued FY25, we expect earnings to recover in the O2C segment, driven by improvement in refining margins,” Motilal Oswal said.

0 Comment